Introducing the blog and updated thoughts on the TIGO thesis

Some history, purpose and analysis of growth prospects

Genesis

I have been posting investing-related thoughts on the platform formerly known as Twitter for more than a decade, but at this point I feel moved to put together some long-form writing and to gather it in an easily accessible place. What has provoked this change of heart for me?

One reason is that I believe that the act of writing long-form and sharing it publicly will force me to put together my thoughts in a way that will make them withstand the ruthless judgment of public opinion. This is a higher bar than writing in my journal and presenting ideas in a haphazard manner to a select group of people with whom I have more or less long-standing relationships. So, hopefully it will introduce another level of rigor to my thinking that would remain perhaps otherwise untapped.

Another reason for writing long-form is that I find that Twitter/X has been, and still is, quite a wonderful place for exchanging ideas. That is, if you are wise enough to filter and curate the experience such that most of the noise doesn’t reach your impressionable mind. My hope is that my writing can make a positive contribution of sorts, and furthermore, act as an advertisement for interesting people to reach out to me with whatever crosses their mind.

To be clear, if you, dear reader, are in possession of something that you think I might be interested in, go forth with your head held high and with great confidence stemming from this desire of mine to be reached, and make your voice heard.

Or, as the author of Escaping Flatland eloquently put it:

”A blog post is a very long and complex search query to find fascinating people and make them route interesting stuff to your inbox.”

This will be one of the purposes of this blog as well.

Telecom focus and interest in Millicom

Over the last few years a lot of my time has been spent trying to understand the telecom industry, as it has been a space characterized by several factors that fit my investing style well: it’s a part of the business world that I have a reasonable chance of understanding, the valuations have been low, there have been a lot of corporate actions and thus, situations where a fresh perspective may yield differentiated insights.

More specifically, my main interest has centered on Millicom, and by extension, the Iliad group of companies. Some of you will have come to know me as a form of sidekick to alwaysinvert, as our interests in this area quickly converged once the company became a takeover target. Since he was already actively publishing on his substack, I felt the proper course of action was to at various times comment, add, or in general bring attention to his work, given the quality of his synthesis.

If you want a go-to source for reading about Millicom, his blog is still unparalleled, and most of what I will be able to contribute on the topic will probably be things provoked by discussions I have had, or am actively engaged in with him. Or, more honestly, insights he figured out, and I, by immense feats of mental gymnastics will appropriate and represent as my own.

Mild rhetorical devices aside, correct attribution when it comes to investment ideas is difficult to accomplish, and I have benefited enormously from the collaboration with him and others, so from my perspective the praise is highly appropriate.

Now, with qualifiers and introductions taken care of, let’s get down to business.

The important questions

While it makes my value investing psyche somewhat uncomfortable, given that the stock has been trading so well recently, the position I will take today is that the setup is still very attractive. My main reason for being positive is that I would answer the three most important questions with regards to future fundamentals in the affirmative.

One assumption I am making here is that the company’s current profitability levels in the core operations are, at minimum, sustainable. Another assumption I am going to make, which is a change from a year or two ago, is that the minority investor’s chances of receiving additional value from potential corporate actions are smaller today. An additional significant factor to keep in mind is the ability of leveraging cash flows in the telecom business.

The conclusion I am brought to — given the current profitability, the ability to leverage that profitability, and the lack of obvious meaningful corporate action beyond what has already been announced — is that the question of growth is the most important area to think about as an investor in Millicom today.

The questions I am interested in can be summarized as follows:

1) Will the company be able to grow in addition to being highly cash flow generative?

2) Will the announced acquisitions create value?

3) Are minority shareholders aligned with the Niel family?

In response to an analyst question about growth, CEO Marcelo Benitez gave this terrific answer, which I posted about at the time:

The company’s plan is: prepaid to postpaid migration, price increases, net adds in the Home business and lowering churn through convergent offerings. Will it work?

Well, looking at more mature markets, the end state is clearly postpaid, bundled offerings. Millicom itself has been growing postpaid subscribers faster than overall mobile subscribers for a long time, so this is just extrapolating global- and company-level trends. On the pricing side, the increased demand for data should logically translate into higher prices over time if competitive dynamics allow for it. The main exception in Millicom’s markets has been Colombia, where prices per GB fell from COP 5,768 per GB in December 2020 before WOM’s entry, to COP 1,753 per GB in December 2024 — a fall of 70%. While WOM has entered restructuring and received financing from new ownership, it seems unlikely to me they will attempt the same level of aggressive competitiveness as in the past.

With regards to fixed broadband net adds, the argument is similar to postpaid mobile; when people can afford it, they seem to want access to fixed broadband. Bundling that access with a mobile subscription makes sense for the customer if they can receive lower rates from their provider, which is made possible economically from the provider side by the lower churn of converged customers. Given that customer acquisition costs are substantial in the telecom business, lowering churn has cost advantages, since fewer customers need to be added on a gross basis to maintain the same level of overall customers. The idea of convergence in order to bring down churn is something the Iliad team have focused consistently on across their businesses, for good reason.

In addition to these organic changes, local currencies have developed favorably lately with the exception of the Bolivar, which will at least boost Q3 numbers in USD terms if nothing drastically changes in the short term.

M&A

The acquisitions can be divided into two categories: in-market consolidation and new markets. In-market consolidation in telecom is normally transformative to market structure, due to the large fixed costs associated with building and maintaining the required networks. When those costs can be spread over a larger amount of customers, the cost of building out the network is lower per customer, but perhaps more importantly, there is one less competitor trying to recover costs spent on developing networks. Since the marginal cost of adding a customer to an existing network is negligible in terms of the network, competition for new customers often becomes intense.

In Colombia, there is no real opposition to the idea of market consolidation today. With the exception of Claro, none of the other market participants have been able to generate sufficient returns needed to motivate further buildouts of network infrastructure. Most of them have either ended up in restructuring or required capital injections from their owners. The economic reality is that for further investment in Colombia to be rational rather than ruinous, scale needs to increase and competitive pressures need to decrease.

The scenario that could be detrimental to Tigo is if there were draconian remedies imposed on the merger in order to protect subscale players. But what is the point of enforcing conditions that would defeat the purpose of consolidation, as one of the main ideas is to create an opposing force to Claro, which through its position of being the sole profitable operator has since long dominated the market? If Tigo were to be limited competitively in some meaningful sense, Claro would have free rein to go after any customer they like, safely knowing that the only competitor able to offer a long term competitive response is held back by regulation.

If Tigo is hamstrung by remedies, not only would they not have the same ability to invest, but the remedies wouldn’t even achieve the ostensible reason for their imposition: to protect smaller players in the market.

The acquisitions in Uruguay and Ecuador were made from a motivated seller, for which the assets being sold were no longer deemed part of their core business, deciding instead that they have other more immediate uses for that capital. Outside of local actors and América Movil, prospective buyers for Latin American telecom assets have been few and far between, creating a favorable supply/demand dynamic for Millicom. Usually, when there is a motivated seller and few potential buyers, that will create an opportunity on the end of the buyer. I think it is safe to assume that Millicom will be able to find areas of improvement in the management of these assets.

Is there any evidence that points to the analysis of the two first questions being correct, you may ask? I would argue yes. The board has somewhat surprised market participants by both returning large amounts of capital and making acquisitions into new geographical areas, all with internally generated funds, and importantly, without pushing leverage more than nominally above their targeted range. If the board or senior management were harboring any doubt towards the task of integrating these new companies into Millicom, the capital allocation doesn’t reveal any such hesitation. I would expect a more cautious approach to capital allocation and their communication to the market, if they thought the outcome was uncertain.

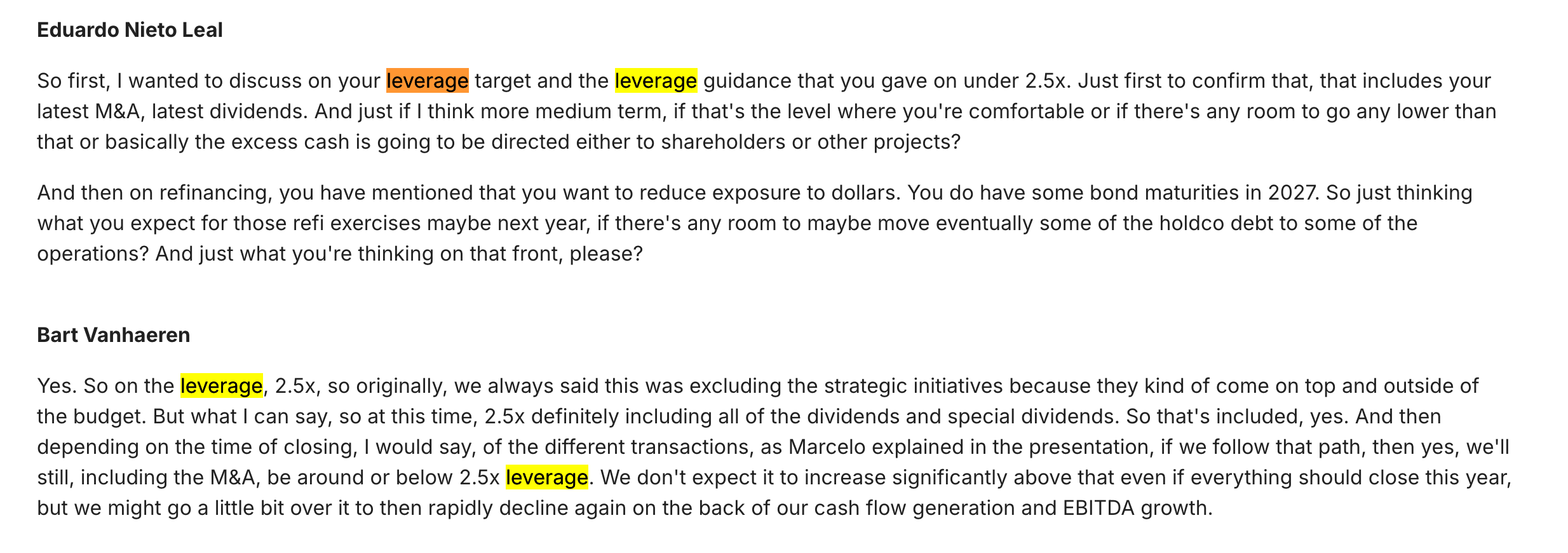

Here’s CFO Bart Vanhaeren on the last earnings call:

They expect leverage to rapidly decline on the back of cash flow generation and EBITDA growth post-acquisitions.

To top it off, Atlas has engaged in a series of options arrangements with three separate banks, which if executed in a way that results in physical settlement of stock would translate into a very aggressive purchase program. I see no plausible reason to assume anything other than that they will end up taking physical settlement of the shares, since their interest lies in increasing their stake in the company for the long term, and they have done so via structured arrangements in the past. Without full certainty, I would assume this is a creative way for them to keep down cost, lower capital requirements, increase optionality and not make their intentions abundantly clear to other market participants that don’t bother to read through the documents or make the effort to understand their intentions. When the guys in Paris are aggressively buying a telecom stock, history tells us that we should pay attention.

Shareholder alignment

As pertains to the third of my three questions, I will try to keep my comments short for the sake of brevity. Of the questions I deem most important, it is probably the one I have the least new thoughts on, which of course doesn’t make it any less important.

It certainly seems to me that Iliad is acting in a manner worthy of celebration for minority shareholders. They have fundamentally transformed the business, they have committed publicly to returning increasing amounts of capital and they are doing all the right moves from my perspective. In addition, if I am not misunderstanding something in the arcane jungle of options trade disclosures, they are now buying exposure to the stock in a manner more aggressive than anything we have seen since the spring of 2023.

Now, this setup of alignment with minority shareholders might partially be a result of Iliad having other, more pressing uses for that capital than a takeover of Millicom, but there is no clear instance of them acting obviously hostile to other shareholders in the past. Rather the opposite, in my estimation.

Still, I periodically enter into bursts of worry about this, since being aligned with Iliad is of supreme importance given their skill in managing telecom assets, both from an operational and a financial standpoint. It is, in fact, at the heart of the investment thesis.

A note on valuation

A lot of the discussion I see with regards to valuing the equity of Millicom is aimed at pinpointing an exact number of free cash flow that the business will generate at some future point, and subsequently determining what an appropriate multiple is to capitalize those cash flows at. For me, this is the wrong approach for forming a basis for decision making on a stock like this. The better approach as far as I am concerned is thinking about what you need to assume for the stock to work out according to your return requirements.

If we anchor to a free cash flow number extrapolated from historical numbers we run the risk of misjudgment in one of two ways; either we overestimate future developments because the decision makers of the business have another agenda (see Iliad in 2021), or we will underestimate future developments because, as the saying goes, great leadership teams tend to surprise you with consistently outperforming your expectations (see Tele2 in 2025).

While having a price target derived from a projected cash flow number multiplied by a customary capitalization factor may provide a sense of control in a situation of decision making under uncertainty, I would argue that it is an illusion of control. Personally, I will opt for the more dynamic model of evaluating incentives, competitive positioning, leadership qualities and macroeconomic exposure and make a judgment call relative to what type outcome is implied in the stock price.

From this perspective, alignment with Iliad is crucial, because if the evaluation of their competencies as operators and financial decision makers is correct, they will most likely exceed reasonable expectations. It lies in the nature of the highly skilled to be able to add value in ways that are difficult to anticipate as a non-expert. If they are consistently able to add value beyond the expectations of market participants, not only will extrapolated cash flow numbers be too low, but the market will rationally reward them with a higher multiple than is customary, which will incorporate some of that ability to generate value.

If you made it all the way here without excessive groaning, I salute you.

Thank you for reading.